Made my day!

(I wrote about this in February.)

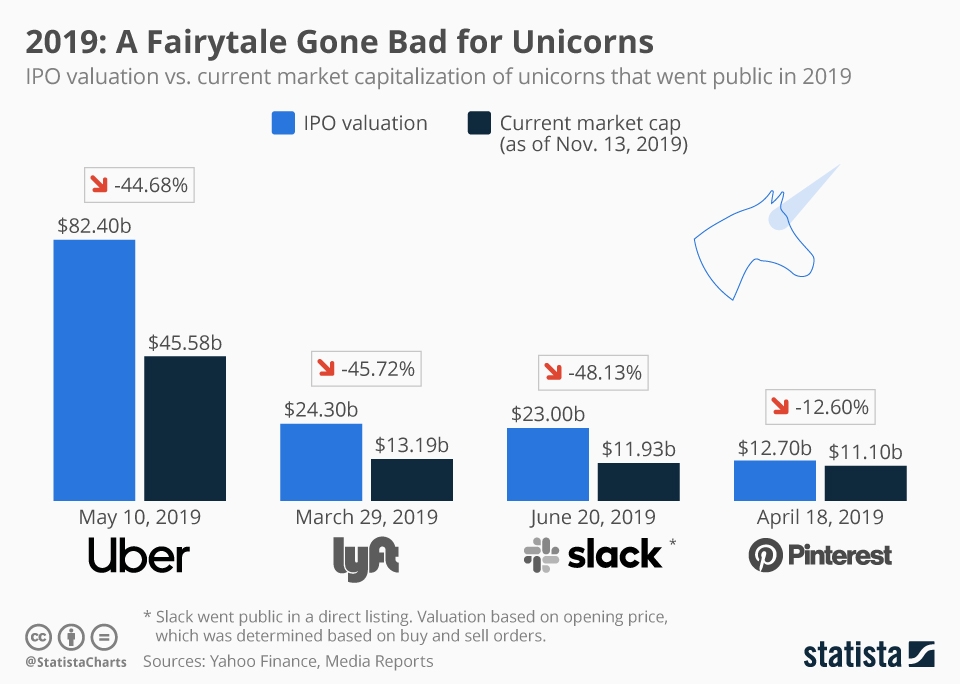

This morning’s Observer column:

Some unicorns have astonishing valuations, which are based on the price that new investors are willing to pay for a share. Uber, for example, currently has a valuation in the region of $80bn (£61bn) and there is feverish speculation that when it eventually goes for an initial public offering (IPO) it could be valued at $120bn (£91bn). This for a company that has never made anywhere near a profit and currently loses money at an eye-watering rate. If this reminds you of the dotcom boom of the late 1990s, then join the club.

There is, however, one significant difference. The dotcom boom was based on clueless and irrational exuberance about the commercial potential of the internet, so when it became clear that startups such as Boo.com and Pets.com were never likely to make a profit, the bubble burst as investors tried to get out. But investors in Uber probably don’t care if it never makes a profit, so long as it gets to an IPO that enables them to cash out with a big payoff. If Uber did go public at a valuation of $120bn, for example, the Saudi royal family alone would have a $16bn (£12bn) payday from their investment.

So what’s going on?

Lovely example from Mark Liberman:

I tried a chapter-opening from a roman policier that I was reading (Yasmina Khadra, Le Dingue au Bistouri): “Il y a quatre choses que je déteste. Un: qu’on boive dans mon verre. Deux: qu’on se mouche dans un restaurant. Trois: qu’on me pose un lapin.”

Google Translate: There are four things I hate. A: we drink in my glass. Two: we will fly in a restaurant. Three: I get asked a rabbit.

Bing Translate: There are four things that I hate. One: that one drink in my glass. Two: what we fly in a restaurant. Three: only asked me a rabbit.

Should be: There are four things I hate. One: that somebody drinks from my glass. Two: that somebody blows their nose in a restaurant. Three: that somebody stands me up.

These mistakes underline some general remaining difficulties. One: the treatment of pronouns. Two: the treatment of idioms that are not common in the bilingual training material. Three: the lack of common sense.

Note that last point.

And, er, where’s the fourth ‘hate’? It’s in neither the original nor the translations.

Yesterday marked the 20th anniversary of Amazon’s IPO. It’s market cap stands today at $459.5 billion. Walmart, meanwhile stands at $229.5 billion. So Amazon is apparently twice as valuable as Walmart.

And yet according to Recode…

Walmart has well more than three times Amazon’s annual revenue, and five times its net income. But Jeff Bezos and Amazon have sold a vision of revenue growth over huge net income figures — and Wall Street has largely bought in.

Also: Amazon employs 341,500 people. Walmart provides jobs for 2.3 million.

Go figure.

This morning’s Observer column.

If one wanted to be critical, the most annoying thing about the current bubble is the way the visions and ambitions of startup founders seem to have narrowed. Many of them claim, of course, that what they want to build is a company that in the long term will transform the world or disrupt a particular market. But in actual fact their strategy is to create a product or a service that is sufficiently interesting or annoying to induce Google, Amazon, Facebook, Yahoo or Microsoft to buy the upstart venture. The poster child for this is WhatsApp, a fine company with a viable business model that did not depend on monitoring users and which was run by a chap who fervently declared his resolve to build a great, sustainable enterprise that treated its users well. And he doubtless believed that right up to the moment that Facebook offered him $19bn. And who can blame him: you only live once, after all.

At the end of the day, though, what’s much more worrying than the spectacle of venture capitalists blowing investors’ money is the fact that everywhere state funding for the kind of long-term, fundamental research that is needed to produce the technologies of tomorrow has been shrinking. The current wave of innovation and economic development enabled by the internet has only come about because 60 years ago the US government funded the project that produced first the arpanet and then the internet.

Private enterprise would undoubtedly have produced computer networks, but it would not have created the free and open platform for “permissionless innovation” that we got as a result of public investment. And we would have all been poorer as a result.

My Observer review of Astra Taylor’s The People’s Platform: And Other Digital Delusions.

The launch of the Mosaic browser in 1993 transformed the internet into a mainstream medium and brought the corporate world online, so from then on the die was cast. What happened is that the two universes effectively merged, so we now live in a strange amalgam of meat- and cyberspace in which the elements of each run riot. A virtual space that once had no crime and no surveillance has become one with an abundance of each; and the “real” world has been destabilised by the astonishing power and properties of networks.

Yet public understanding of the implications of this convergence lags some way behind the emerging reality, which is why we need books like this. Astra Taylor is a talented documentary-maker who was dismayed by the way her work was appropriated and pirated online. But instead of fuming silently in her studio, she set out to seek an understanding of the paradoxical world that the merging of cyberspace and meatspace has produced. What she finds is a world which is, on the one hand, hooked on an evangelical narrative about the liberating, empowering, enlightening, democratising power of information technology while, on the other, being increasingly dominated and controlled by the corporations that have effectively captured the technology.

The big question about the net was always whether it would be as revolutionary as its early evangelists believed. Would it really lead to the overthrow of the old, established order? We are now beginning to see that the answer is: no. We were intoxicated by the exuberance of our own evangelism. “From a certain angle,” writes Taylor, “the emerging order looks suspiciously like the old one.” In fact, she concludes, “Wealth and power are shifting to those who control the platforms on which all of us create, consume and connect. The companies that provide these and related services are quickly becoming the Disneys of the digital world – monoliths hungry for quarterly profits, answerable to their shareholders not us, their users, and more influential, more ubiquitous, and more insinuated into the fabric of our everyday lives than Mickey Mouse ever was. As such they pose a whole new set of challenges to the health of our culture.”

This morning’s Observer column.

As the “big data” bandwagon gathers steam, it’s appropriate to ask where it currently sits on the hype cycle. The answer depends on which domain of application we’re talking about. If it’s the application of large-scale data analytics for commercial purposes, then many of the big corporations, especially the internet giants, are already into phase four. The same holds if the domain consists of the data-intensive sciences such as genomics, astrophysics and particle physics: the torrents of data being generated in these fields lie far beyond the processing capabilities of mere humans.

But the big data evangelists have wider horizons than science and business: they see the technology as a tool for increasing our understanding of society and human behaviour and for improving public policy-making. After all, if your shtick is “evidence-based policy-making”, then the more evidence you have, the better. And since big data can provide tons of evidence, what’s not to like?

So where on the hype cycle do societal applications of big data technology currently sit? The answer is phase one, the rapid ascent to the peak of inflated expectations, that period when people believe every positive rumour they hear and are deaf to sceptics and critics…

The word “legacy” crops up a lot in discussions about innovation in cyberspace, so it was good to find thoughtful essay about it by Stephen Page, current CEO of Faber & Faber, the eminent publishing house of which TS Eliot was famously a Director.

In any revolution, language matters. One powerful word in the digital revolution is “legacy”. There is a conscious attempt to employ the word pejoratively, to suggest that existing media businesses – publishers, in the case of books – are going to fail to make the leap to a new world.In common usage, the first meaning of legacy is an inheritance, or something handed down from the past. A second meaning, more specific and recent, denotes technological obsolescence, or dramatic business-model shift. These two meanings have been fused to imply inevitable irrelevance for those with history, especially in media. This is a sleight of hand that would be sloppy if it wasn’t so considered.

Let’s deal with technological obsolescence. Media businesses are not technology businesses, but they can be particularly affected by technology shifts. I run a so-called legacy publishing house, Faber & Faber. Most of our business is based on licensing copyrights from writers and pursuing every avenue to find readers and create value for those writers. We are agnostic about how we do this. For our first 80 years, we could only do it through print formats (books); now we can do it through books, ebooks, online learning (through our Academy courses), digital publishing (such as the Waste Land app) and the web. Technology shifts have tended to result in greater opportunity, not less.

Implicit, I suppose, in the pejorative use of the term legacy is that we at Faber, like other publishers, don’t get it – “it” being the new economy, the new rules. There is something in this, of course. It’s harder to transform an existing business into one with a new culture and cost structure than to start afresh. Any existing business, no matter what old-world strength it has, will fail if it is not bold enough to attack its own DNA where necessary. The ailing photography firm Eastman Kodak is widely cited as a recent example of this phenomenon. But this is business failure due to cultural stasis. There is nothing inevitable in failure for existing businesses, but they have particular issues to figure out: simply adhering to old business practices will lead to failure. Failure will not be because of technology, but through failure to react to technology. In fact, it could be regarded as squandering the opportunity of a beneficial legacy.

He’s right about the two meanings. A legacy can be a source of mindless complacency — the kind of mindset one finds in the trust-fund Sloanes who hang out in Belgravia and Chelsea. But it can also be a source of strength — as in the case of Faber, who seem to me to be approaching the challenges of digital technology with imagination and vision. For example, the wonderful Waste Land App produced by my friend Max Whitby and his colleagues at TouchPress required access to the Eliot papers and rights held by Faber. So they used their ‘legacy’ to add value to a digital product in a distinctive and valuable way.

But others legatees in the publishing (and other content industries) have viewed their inheritances in different and less imaginative ways. Think, for example, of the way Stephen Joyce has relentlessly used his control of the Joyce estate to prevent imaginative uses of his grandfather’s works. (Mercifully, Ulysses is now finally out of copyright and therefore beyond Stephen’s baleful reach, which is what has enabled TouchPress to embark on an imaginative App based around a new translation that will come out later this year.). Or of the way some legatees have viewed their inheritances as guarantees that the digital revolution will never threaten their hold on a market.

Still, Mr Page is right: “legacy” is too often used as a term of patronising abuse by tech evangelists who think that they have “the future in their bones” (as C.P. Snow put it in his famous Rede Lecture all those years ago.)

Insightful Guardian column by Dean Baker.

Of course, Facebook is unlikely to go out of business, but it is certainly possible that its business model is not sufficiently robust to justify a position among corporate America’s elite in market capitalization. A year or two down the road, it may well turn out that its share price ends up at half or less of its IPO price (at time of writing, it is already off 13%).

In this case, there will have been an enormous transfer of wealth from the purchasers of Facebook stock to those able to cash out following the IPO. This will make many of those on the inside of the company fantastically wealthy. However, much of their wealth would not result from making a good product that society valued; rather, it came from being part of a successfully hyped company.

These insiders benefited from the ability of Mark Zuckerberg and his colleagues to convince investors that Facebook had much more profit potential than, in fact, was true. This ability to hype a product (in this case, company stock) can be an incredibly valuable skill, but it provides nothing of value to society. In that way, it is similar to the skills of Fabrice Tourre (aka “Fabulous Fab”), who was apparently very skilled in putting together complex mortgage derivatives for Goldman Sachs that were designed to fail.

ALSO: Interesting WSJ video conversation about Facebook’s feeble showing on smartphones.

And now this story:

Financial regulators are to investigate whether the banks in charge of Facebook’s initial stock offering broke the rules by selectively releasing negative news about the company before shares went on sale.

The financial industry regulatory authority (Finra) is looking into allegations that Morgan Stanley and other banks released reduced revenue forecasts for Facebook to big investors – but not the general public – before Friday’s IPO. Such activity could constitute a violation of securities law.

This morning’s Observer column.

So Facebook has bought Instagram, a company with a single product – a photosharing app – for $1bn in cash and (FB) shares. Just to put that in context, Instagram has been in existence for 18 months, employs 13 people, has 30 million users and has had a grand total of $7m in investment funding. Oh, and it has precisely zero dollars in revenue.

Sound familiar?

There’s been lots of really interesting commentary about the Instagram deal. Writing in the FT, John Gapper made two interesting points:

And Frederic Filloux, one of my favourite commentators, is also sceptical about the deal — and about facebook generally. “When I read the news of the Instagram acquisition”, he writes, “I wondered: Imagine Facebook already trading on the Nasdaq; how would the market react? Would analysts and pundits send the stock upward, praising Zuckerberg’s swiftness at securing FB’s position? Or, to the contrary, would someone loudly complain: What? Did Facebook just burn the entire 2011 free cash-flow to buy an app with no revenue in sight, and manned by a dozen of geeks? Is this a red-flag symptom of Zuckerberg’s mental state?”

Other points Filloux makes:

LATER: Andy Baio has made an interesting attempt to work out an empirical rationale for the price Zuckerberg paid for his new toy.