“The Secret Service is the only law-enforcement agency that will get into trouble if a black man gets shot.”

American comedienne Cecily Strong at Saturday’s 2015 White House Correspondents’ Dinner.

“The Secret Service is the only law-enforcement agency that will get into trouble if a black man gets shot.”

American comedienne Cecily Strong at Saturday’s 2015 White House Correspondents’ Dinner.

The thing about neoliberalism is that it’s a machine for producing and amplifying inequality. In other words, inequality is not a regrettable and inevitable byproduct of an otherwise admirable economic doctrine: it’s what the system is designed to do. Or, as programmers would say, it’s a feature, not a bug.

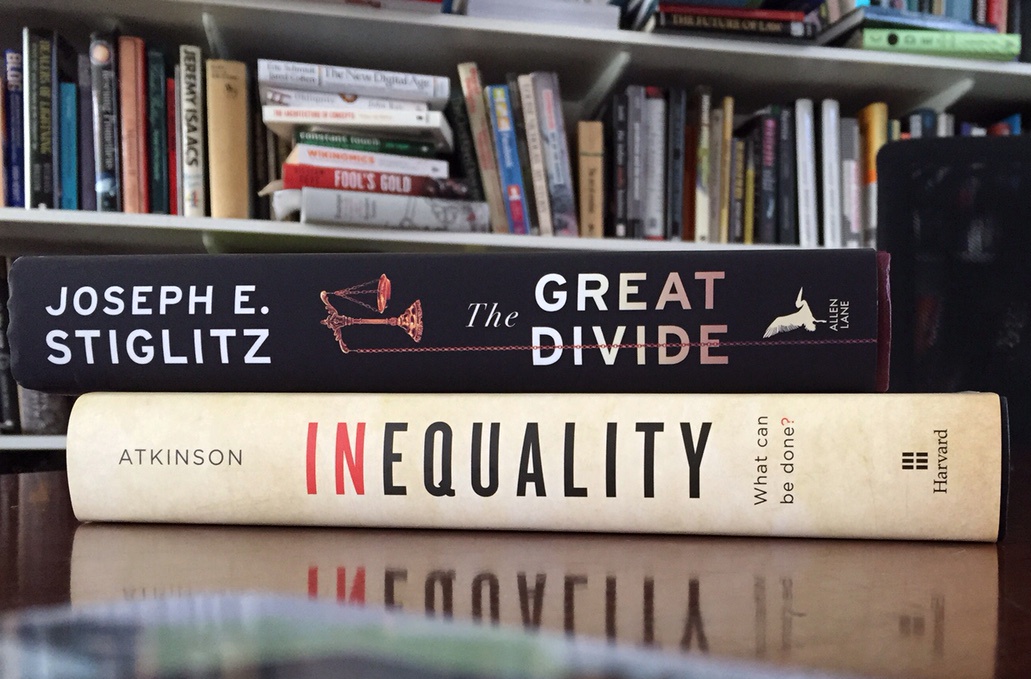

Hot on the heels of Thomas Piketty come two terrific books. Tony Atkinson has been studying inequality for decades, and his new book

challenges the conventional wisdom that there’s nothing we can do about rising inequality. He sets out a comprehensive set of policies that could bring about a real shift in income distribution in developed countries. To reduce inequality, he says, we need to go beyond taxing the wealthy (though we should also do that). Atkinson thinks we need new ideas in four other areas: technology, employment, social security, the sharing of capital. If I had to summarise the book in a phrase, I’d say it was the embodiment of informed optimism.

Joe Stiglitz has been writing about inequality for ages too, and his new book is a set of essays that expand on the diagnosis he proposed in an earlier best-seller, The Price of Inequality

. Like Atkinson, Stiglitz thinks that we could reduce inequality if we were smart and determined enough. The conventional neoliberal wisdom which says that we have to choose between economic growth and fairness is, he thinks, bunkum. I agree. Trouble is, none of our politicians do.

No matter what you think about Google, it’s an astonishing project. Also I can’t think of another company that could — or would — attempt it.

” Facebook is interested in “digital inclusion” in much the same manner as loan sharks are interested in “financial inclusion”: it is in it for the money.”

Evgeny Morozov, writing in the Observer, April 26, 2015.

70 years ago yesterday US and Soviet troops met at the river Elbe, which then became the dividing line for a defeated Germany. Note that the GIs are the ones with cigarettes.

Like many people, I’m puzzled by Hilary Clinton. I thought she was a good US Secretary of State. But I’ve been suspicious of her preparations to run for the presidency, which looks awfully like a formulaic enterprise from an operating manual laid down two decades ago. And she’s clearly the Democratic Establishment’s candidate. But I’ve no idea what she’s like as a person, which is why this piece by Bertrand-Henry Lévy (who has met her three times) is interesting. Especially this bit:

Sometimes her expression is briefly clouded by a streak of stifled pain, obstinate and not wholly contained. Five years earlier, she was the most humiliated wife in America, a woman whose private life was thrown open – fully and relentlessly – to public scrutiny. So she can talk national and international politics until she is blue in the face. She can sing the praises of John Kerry, whom her party has just nominated in an effort to deny George W. Bush a second term. And she can expound on her role as the junior senator from New York. Still, there persists an idea that I cannot push out of my head, and that I enter into the travel journal that I am writing for The Atlantic.

The idea is this: to avenge her husband and to take revenge on him, to wash away the stain on the family and show what an unblemished Clinton administration might look like, this woman will sooner or later be a candidate for the presidency of the United States. This idea brings to mind Philip Roth’s The Human Stain, published a year after the Senate acquitted her husband of perjury and obstruction-of-justice charges, with its searing portrait of how indelible even an undeserved blot on one’s reputation can be. She will strive to enter the Oval Office – the theater of her inner, outer, and planetary misery – on her own terms. And the most likely outcome, my article will conclude, is that she will succeed.

Wikipedia is one of the wonders of the world, which is why I donate to it as well as use and edit it. But until now I’d never thought of listening to the music that it makes.

Unmissable. Try it.

If I were an American undergraduate I’d say it was awesome, but now I discover that Wikipedia has no entry for that usage.

This morning’s Observer column:

At first sight, it looked like an April Fools’ story. The US Department of Justice is seeking to extradite a day-trader from Hounslow to stand trial on charges that he brought the US stock market briefly to its knees on 6 May 2010. Navinder Singh Sarao is accused of using a computerised share-trading program to manipulate the market for S&P 500 futures contracts on the Chicago Mercantile Exchange, thereby adding (so the prosecution alleges) to wider selling pressure that caused the Dow Jones industrial average to plunge briefly by 6% before bouncing back.

In that short interval, stocks in huge companies such as Procter & Gamble dropped by 25% and established companies such as General Electric and Accenture briefly traded as penny shares. The British courts, not to mention the rest of us, are invited to believe that this mayhem was caused by a 36-year-old geek in the bedroom of his parents neat semi-detached house under the Heathrow flight path.

There are, it seems to me, only two possible interpretations of this. One is that Mr Sarao is indeed responsible for the chaos. The other is that the US authorities have no real idea who is responsible, but need to make an example of somebody and Mr Sarao will do nicely. Either way, we are left with a really alarming conclusion, namely that we have constructed a world that is totally dependent on systems that are a) astonishingly fragile and unpredictable, and b) incomprehensible not only to the average citizen but to those who are supposed to regulate them…

![]()

YouTube turns ten this year. ArsTechnica has a nice post that reflects on its history and its significance.

Excerpt:

The site has become so indispensable that it feels like a basic part of the Internet itself rather than a service that lives on top of it. YouTube is just the place to put videos, and it’s used by everyone from individuals to billion-dollar companies. It’s obvious to say, but YouTube revolutionized Web video. It made video uploading and playback almost as easy as uploading a picture, handled all the bandwidth costs, and it allowed anyone to embed those videos onto other sites.

The scale of YouTube gets more breathtaking every year. It has a billion users in 61 languages, and 12 days of video are uploaded to the site every minute—that’s almost 50 years of video every day. The site just continues growing. The number of hours watched on YouTube is up 50 percent from last year.

It’s easy to forget YouTube almost didn’t make it. Survival for the site was a near-constant battle in the early days. The company not only fought the bandwidth monster, but it faced an army of lawyers from various media companies that all wanted to shut the video service down. But thanks to cash backing from Google, the site was able to fend off the lawyers. And by staying at the forefront of Web and server technology, YouTube managed to serve videos to the entire Internet without being bankrupted by bandwidth bills…

Great read. Recommended.

Fascinating piece in Slate.

At 7.32pm on March 27, Dama Mattioli, a reporter on the Wall Street Journal, tweeted thus:

“Intel is in talks to buy Altera. Deal would be largest in Intel’s history. Scoop w/ @danacimilluca coming to http://WSJ.com $ALTR”

Seth Stevenson of Slate recounts what happened next:

Quicker than any human seemingly could have done it, someone—or rather something—bought $110,530 worth of cheap options on Altera, a company that makes digital circuits.* Over the next several minutes and until the end of the day, as humans digested Mattioli’s takeover rumor at human speed, Altera’s stock price rose. When all was said and done, those cheap options had resulted in a $2.4 million profit. Speculation immediately centered on the idea that an automated program (a “bot”) had scanned the tweet, interpreted its meaning, and instantly bought those options based on an algorithm. The robot had read the tweet and made a killing on it before anyone knew what was going on.

In fact a Reuters report found that the trade in question was made a full 19 seconds before the tweet appeared. In a way, though, that only makes the story even more interesting. The WSJ has a policy of putting news on its own newswire before it goes on Twitter and it turns out that the trades occurred a mere second after news of the possible deal appeared on Dow Jones Newswires, and before Altera’s shares were halted.

Yep. A second.

Which means — or at any rate suggests — that an algorithm ‘read’ the news headline and acted to buy short-term options on Altera shares. Which is yet another pointer to what it happening to stock exchanges.