The Blackrock Blog points out that something strange is going on in the investment world.

The Blackrock Blog points out that something strange is going on in the investment world.

MSCI and S&P are updating their Global Industry Classification Standards (GICS), a framework developed in 1999, to reflect major changes to the global economy and capital markets, particularly in technology.

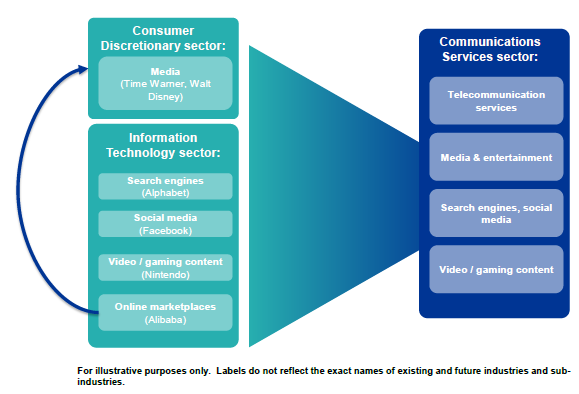

Take Google, a company long synonymous with “tech” and internet software. Google parent Alphabet derives the bulk of its revenue from advertising, but also makes money from apps and hardware, and operates side ventures including Waymo, a unit that makes self-driving cars. Decisions about what makes a “tech” giant are not as simple as they once were.

The sector classification overhaul, set in motion last year, will begin in September and affect three of the 11 sector classifications that divide the global stock market. A newly created Communications Services sector will replace a grouping that is currently called Telecommunications Services. The new group will be populated by legacy Telecom stocks, as well as certain stocks from the Information Technology and Consumer Discretionary categories.

What does this mean?

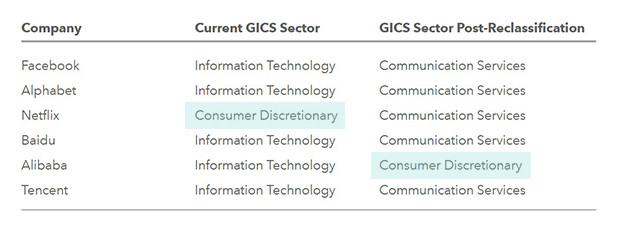

Facebook and Alphabet will move from Information Technology to Communications Services in GICS-tracking indexes. Meanwhile, Netflix will move from Consumer Discretionary to Communications Services. None of what the media has dubbed the FANG stocks (Facebook, Amazon.com, Netflix and Google parent Alphabet) will be classified as Information Technology after the GICS changes, perhaps a surprise to those who think of internet innovation as “tech.” The same applies to China’s BAT stocks (Baidu, Alibaba Group and Tencent). All of these were Information Technology stocks before the changes; none will be after.

Or, in a tabular view:

This change is probably only significant for index funds, but still, it must rather dent the self-image of the ‘tech’ boys to be categorised as merely “communications services”!